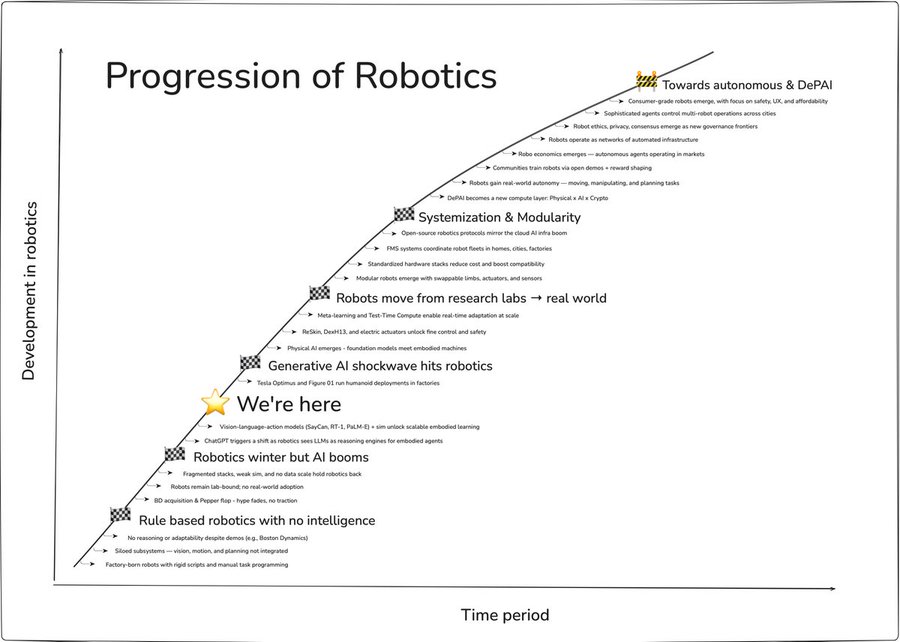

Robotics stack & the Bill of Materials (BOM)

All about robotics stack + BOM - probably one of the most important metrics to track in robotics

Humanoid-robot economics look messy to understand until you zoom into the bill of materials (BOM).

BOM isn’t just a cost sheet, but technically acts a diagnostic tool for identifying:

which subsystems dominate cost vs. differentiation

where integration complexity creates or erodes leverage

how software layers compress cost over time

what forms of IP (mechanical, data, model) retain margin

where supply chain proximity drives iteration speed

This makes the BOM a practical framework for builders, investors, and researchers that reveals everything: to reason about performance bottlenecks, unit economics, and leverage points.

It can tell you why some companies scale like SaaS - and others get stuck in hardware hell.

Let’s understand this across the robotics stack 👇🏻

At the base of every robot is actuation – and that’s where nearly half the cost sits (currently).

Motors, gearboxes, torque systems: these parts are heat-sensitive, hard to miniaturize, and harder to replace. But they’re also strategic strongholds. Vendors like LeaderDrive, Harmonic Drive, and Beite dominate this layer with hard-to-copy IP. They are hardware moats – built on:

tight tolerances

supply chains

decades of iteration

If you control actuator design, you control a robot’s core physics.

But moving up the stack, and the leverage flips.

Compute, sensors, and models only take ~10% each of the BOM. But they increasingly define adaptability, autonomy, and performance. Chips are cheap compared to torque systems - but paired with the right stack, they compound fast.

That’s why companies like NVIDIA don’t just limit themselves to shipping silicon. They own the simulation tools (Isaac), the foundation models (GR00T), and the fleet-learning systems that make robots smarter over time.

Here’s the shift:

Actuation drives cost and complexity

Software drives learning and margin

Sensing and power are bottlenecks but increasingly commoditized

Cost ≠ Commodity

A low BOM doesn’t always mean high margin. A high BOM doesn’t always mean low defensibility.

Here’s the real split:

High BOM + high IP → hardware moat (e.g. gear and actuator vendors)

Low BOM + model/data ownership → software moat (e.g. GR00T stack)

High BOM + low IP → worst of both worlds (commodity assemblers)

The BOM is a lens into margin strategy - whether you’re scaling like SaaS or stuck in supply chains.

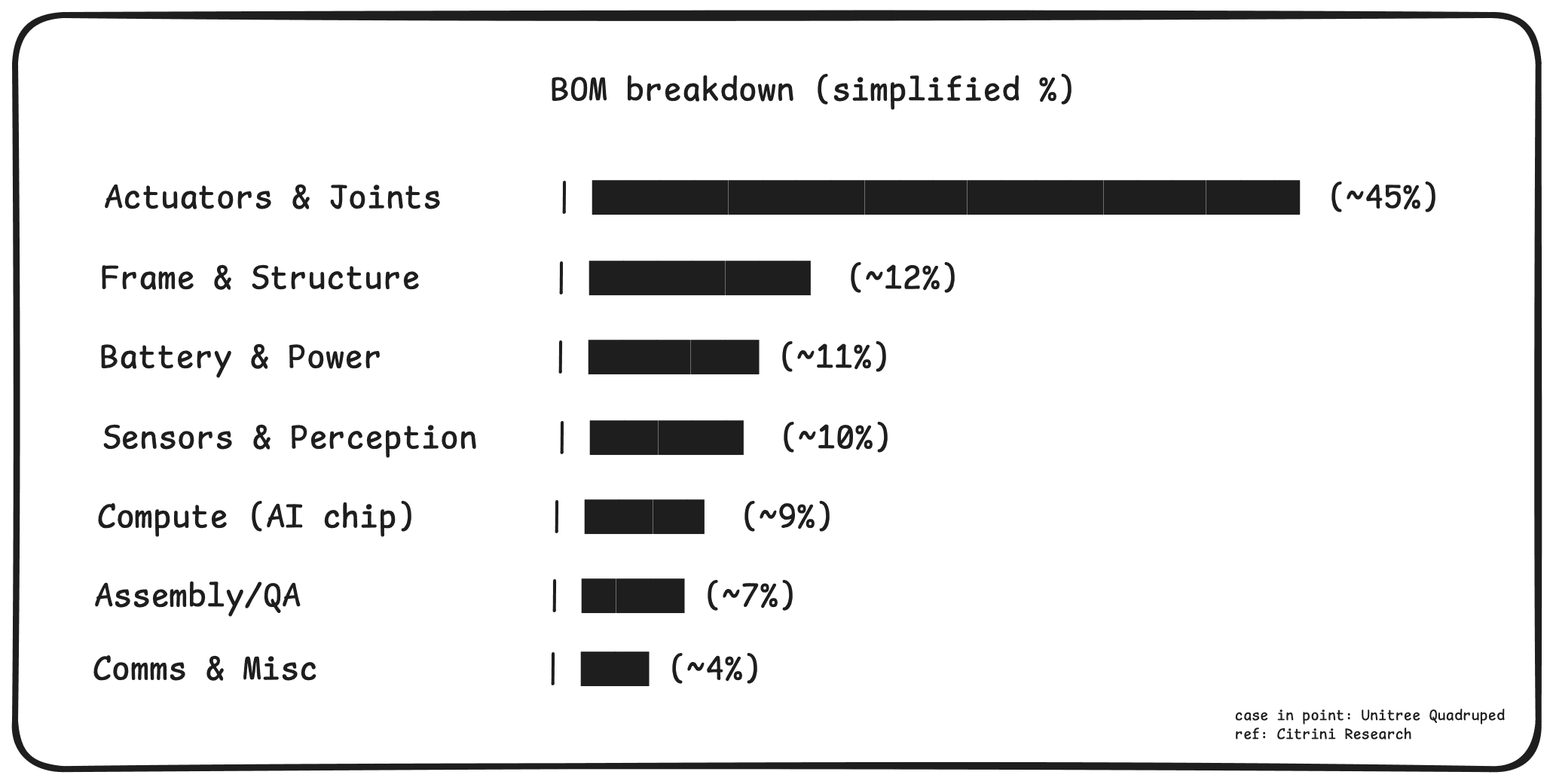

Case study: Unitree’s $16K humanoid

Unitree didn’t get to a low-cost humanoid by revolutionizing AI. It got there by engineering the BOM:

Sourcing actuators locally (cheaper motors)

Skipping advanced sensors like multi-plane LiDAR

Using Jetson compute not custom silicon

No radical architecture changes. Just smart cost control in the subsystems that matter.

Here's a high level breakdown of the BOM for Unitree's Quadruped:

Integration = Margin

Hardware margins are thin, unless you own tight integration or precision complexity.

If a company makes its own actuators and tunes torque curves for behavior, it’s defensible - even with high COGS. If they don’t, they’re just assembling parts.

Meanwhile, if a company owns the software stack, margins scale like code:

Fleet-level learning loops

API-style unit economics

Lower per-unit cost over time

Geography is strategy

Over 90% of Unitree’s suppliers sit within hours of Hangzhou. That’s not a coincidence, it’s a moat.

Local sourcing → lower cost, faster iteration, tighter integration.

Western companies often lack this supply chain density, which slows them down and raises costs.

What’s not in the BOM matters more

You won’t see fleet logs, ROS tuning data, or simulation policies on a BOM sheet - but these are the (upcoming) edge

Data fuels better models → better autonomy → more usage → better data

Whoever owns the data loop might win long-term.

Cutting BOM costs doesn’t guarantee margin gains - in commoditized layers, savings often pass through to the buyer. Without IP or integration advantage, cost-down just accelerates price pressure.

This dynamic is best illustrated in the BOM share vs. margin chart:

Actuation → high cost, high moat, low margin

Compute → low cost, high leverage, high margin

Comms & frame → low cost, low margin, low moat

Sensors → medium cost, increasingly commoditized

Strategic control isn’t purely about spending more, but actually about owning the right layers.

So the BOM becomes a proxy for margin profile:

High BOM, high defensibility → gear/motion IP

Low BOM, high defensibility → model/data IP

High BOM, low defensibility → trapped in the middle

As robotics systems will evolve, I feel BOM will offer a uniquely grounded lens to assess technical constraints, economic structure, and strategic leverage of the robotics stack.